Unified Platforms: The Engine for MENA’s Next Fintech Leap

MENA’s fintech market is booming but fragmented. Discover how unified, API-first platforms are driving the shift from isolated apps to integrated ecosystems.

MENA’s fintech market is booming but fragmented. Discover how unified, API-first platforms are driving the shift from isolated apps to integrated ecosystems.

Subscribe now for best practices, research reports, and more.

The Middle East and North Africa (MENA) region stands at a critical juncture in its financial evolution. We have passed the initial phase of rapid digital adoption, characterised by a surge in mobile wallets, challenger banks, and regulatory sandboxes. The sheer velocity of fintech growth in hubs like Riyadh, Dubai, and Cairo is undeniable. However, velocity without cohesion creates friction.

The current landscape is increasingly defined by fragmentation. We see islands of innovation a brilliant payment app here, a digital lending platform there disconnected from the broader banking ecosystem. For C-Suite leaders and technical architects operating in the region, the strategic imperative has shifted. The next leap in growth will not come from launching another standalone app. It will come from building Unified Platforms that weave these disparate threads into a seamless financial fabric.

Despite high mobile penetration and a young, tech-savvy demographic, the underlying infrastructure of MENA’s financial sector remains siloed. Many incumbent banks are burdened by legacy core systems that struggle to communicate with agile fintech partners. Conversely, fintechs often lack the balance sheet and regulatory clearance to offer full-suite banking services.

This creates a "spaghetti architecture" of point solutions. A consumer might use one app for remittances, another for savings, and a traditional bank account for salary deposits, with no interoperability between them.

For financial institutions, this fragmentation manifests as "Innovation Debt." Integrating a new partner or launching a cross-border payment service requires custom, hard-coded connections that are brittle and expensive to maintain. This stifles agility and keeps the cost of customer acquisition artificially high.

To unlock the true potential of the MENA market, institutions must pivot from an "App-First" mindset to a "Platform-First" strategy.

A Unified Platform is not a super-app in the frontend sense alone; it is a backend orchestration layer. It acts as a central nervous system that connects core banking ledgers, third-party fintechs, payment rails, and regulatory reporting engines.

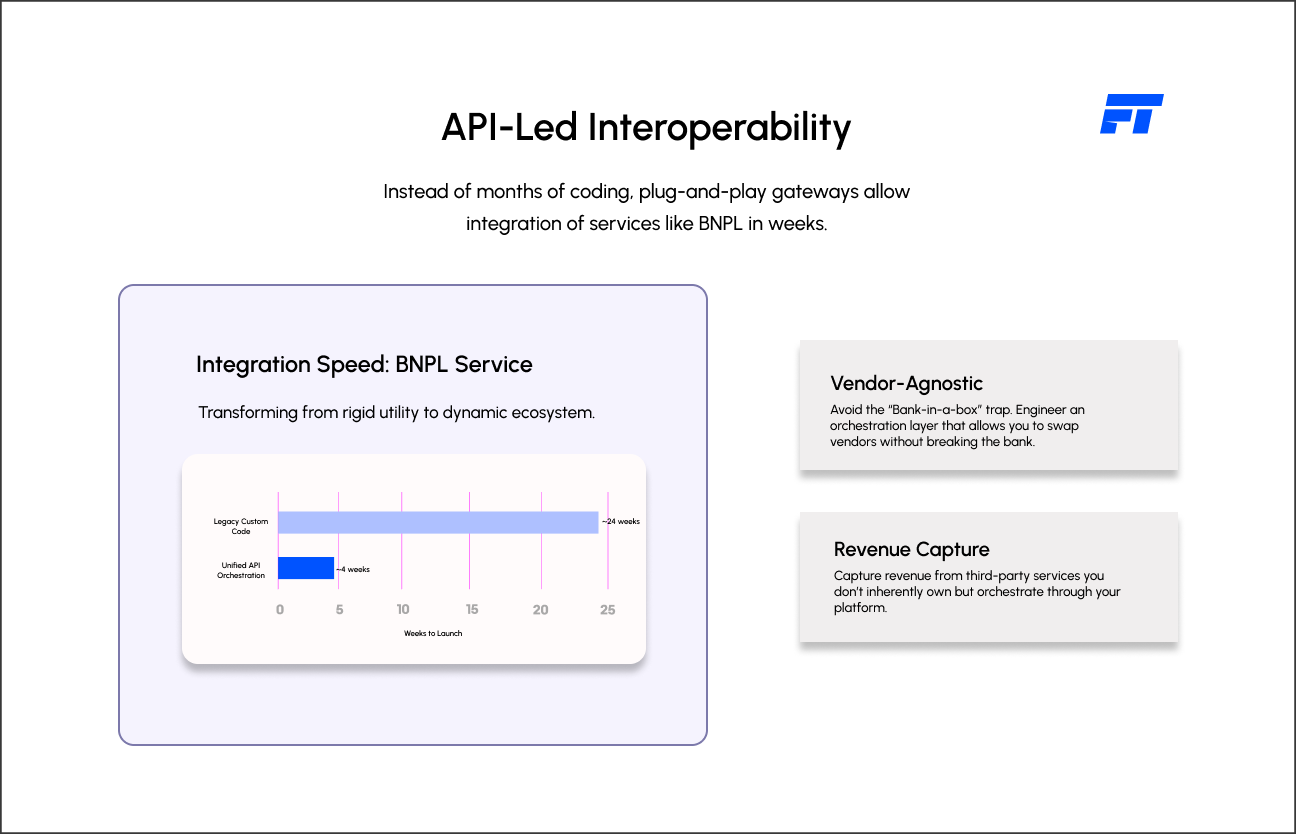

At Fyscal Technologies, we advocate for a vendor-agnostic approach to this unification. Rather than purchasing a monolithic "bank-in-a-box" solution that locks you into a single vendor’s roadmap, we engineer orchestration layers using open APIs. This allows you to plug in the best-in-class KYC provider from Egypt, a payments engine from the UAE, and a core ledger from Europe, all functioning as a single, cohesive unit.

The technical backbone of a unified platform is a robust API strategy. In markets like Saudi Arabia and Bahrain, Open Banking regulations are already mandating this connectivity. However, compliance is merely the baseline. The strategic opportunity lies in API Orchestration.

Instead of building direct, one-to-one connections between your bank and every fintech partner, a unified platform uses an API Gateway to standardise data exchange. This allows for "Plug-and-Play" integration.

For example, a bank can integrate a Buy Now, Pay Later (BNPL) service into its mobile app in weeks rather than months. This interoperability transforms the bank from a rigid utility into a dynamic ecosystem, allowing it to capture revenue from services it does not inherently own.

One of the unique challenges in MENA is regulatory diversity. The compliance rules in the GCC differ significantly from those in North Africa. A fragmented infrastructure forces institutions to build separate compliance stacks for each jurisdiction, which is operationally inefficient.

A unified platform centralises RegTech capabilities. By treating compliance as a shared service within the platform, institutions can automate Know Your Customer (KYC) and Anti-Money Laundering (AML) checks across all product lines.

This "Compliance by Design" approach ensures that whether a customer is taking a micro-loan or sending a remittance, the regulatory logic is applied consistently. It reduces the risk of human error and allows institutions to scale across borders without rebuilding their risk management framework from scratch.

The ultimate promise of MENA’s fintech leap is financial inclusion. A significant portion of the region’s population, particularly Small and Medium Enterprises (SMEs), remains underbanked. The primary barrier is a lack of credit history.

Unified platforms solve this by aggregating data. When a platform connects banking data with telecommunications usage, merchant payments, and logistics data, it creates a rich, alternative credit profile.

For decision makers, this unlocks a massive, previously unserviceable market segment. By leveraging AI within a unified platform to analyse this aggregated data, banks can offer personalised credit products to SMEs with managed risk. This shifts the business model from asset-backed lending to data-backed lending.

Transitioning to a unified platform architecture offers quantifiable returns:

The fragmentation of MENA’s current fintech landscape is a growing pain of rapid digitisation. The institutions that will define the region’s future are those that recognise the need for cohesion.

Building a unified platform is not about buying software; it is about architectural sovereignty. It is about designing a system that is resilient enough to handle legacy demands and agile enough to power the future. Fyscal Technologies helps financial institutions engineer this freedom, ensuring that your platform powers your growth rather than limiting it.

Ready to explore how Fyscal Technologies can help you achieve this?

.png)

.svg)